Because you need money to make money

How has the pandemic affected credit card debt? The answer may surprise you. Credit card debt plummeted during the first quarter of 2021. According to the Federal Reserve Bank of New York, credit card balances declined by $49 billion during early 2021. Here are some more statistics on credit card debt:

Credit card default rates have decreased since the Great Recession, where rates were at 6.7 percent. However, only 48 percent of credit card users make the minimum payments on their cards, causing debt to roll over to the next month. This makes it more difficult to pay off their debts.

As debt grows, it is important to practice responsible spending and payment methods. Letting your debt constantly roll over into the following months is not a smart or responsible way to handle your money. Things can get out of hand quickly, and your debt will only increase. Having some debt is normal, but too much can be a financial burden for years to come if you do not practice good financial habits and do not spend your money wisely.

Using a credit card with a high interest rate is even riskier, so it is vital to pay off the debt before you are charged with a large interest percentage on top of your current debt. Your credit score will suffer if you do not pay off your credit card on time each month. The higher your utilization (the amount of credit you use compared to the amount of credit you have), the lower you credit score will be. The sooner you take care of your debt, the sooner you will repair your credit score and get back on track to buying a car, house, or another important purchase.

According to Experian Consumer Credit Review, the average American has four credit cards. If you are able to manage your credit cards, you can qualify for maximum rewards, interest-free financing, and annual statement credits. While having more than one credit card is useful, you should always watch your credit score and your finances closely, as too many credit cards can lower your score and cause you to spend more, which means more potential debt. Just applying for a credit card account can lower your credit score by five points, so it’s not always a smart move to make if you are trying to improve your credit.

Credit card debt statistics:

States with most credit cards:

States with the fewest credit cards:

Source: Lexington Law

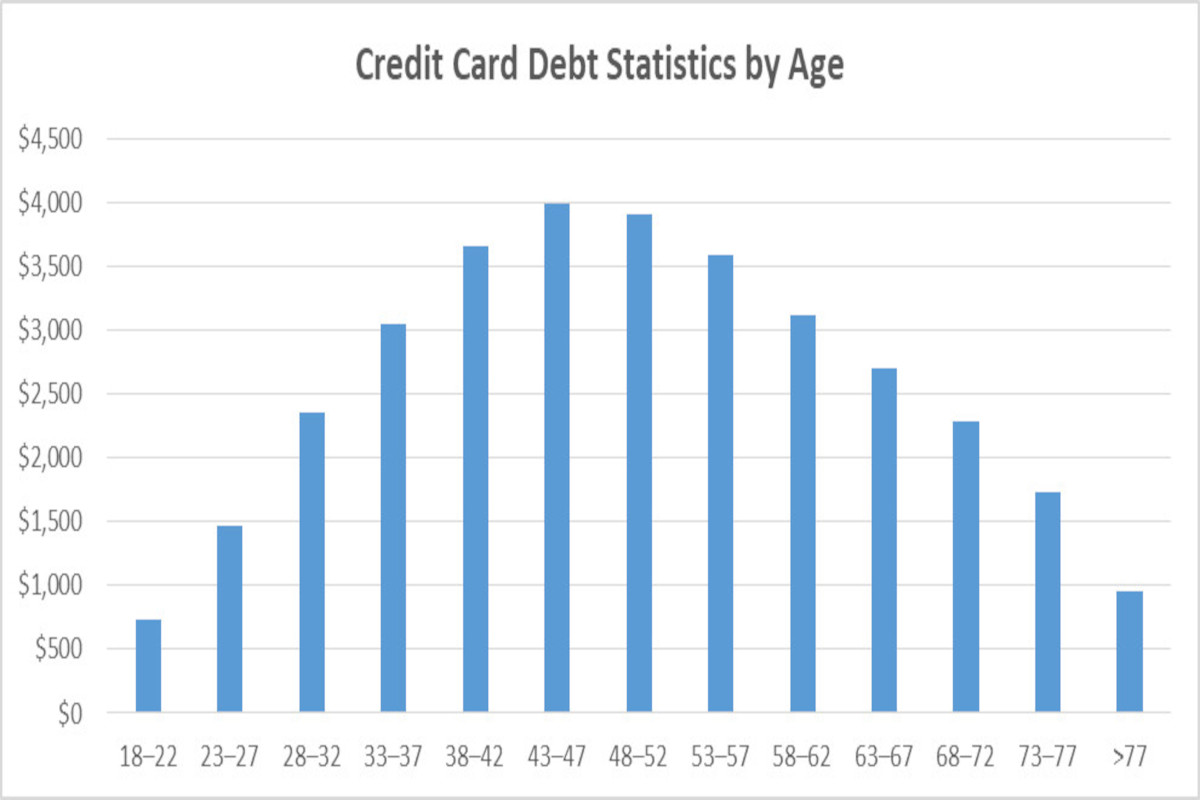

Those aged 18-22 carry the least amount of credit card debt since they are least likely to have credit cards and have the least chance of attaining a high-balance credit line. In contrast, 43-47 year olds have the highest amount of credit card debt. Read below to see the statistics on credit cards by age:

The data below shows that Generation X and Baby Boomers have the greatest amount of credit card debt. Since these groups tend to have a higher income, they spend more money than other generations do.

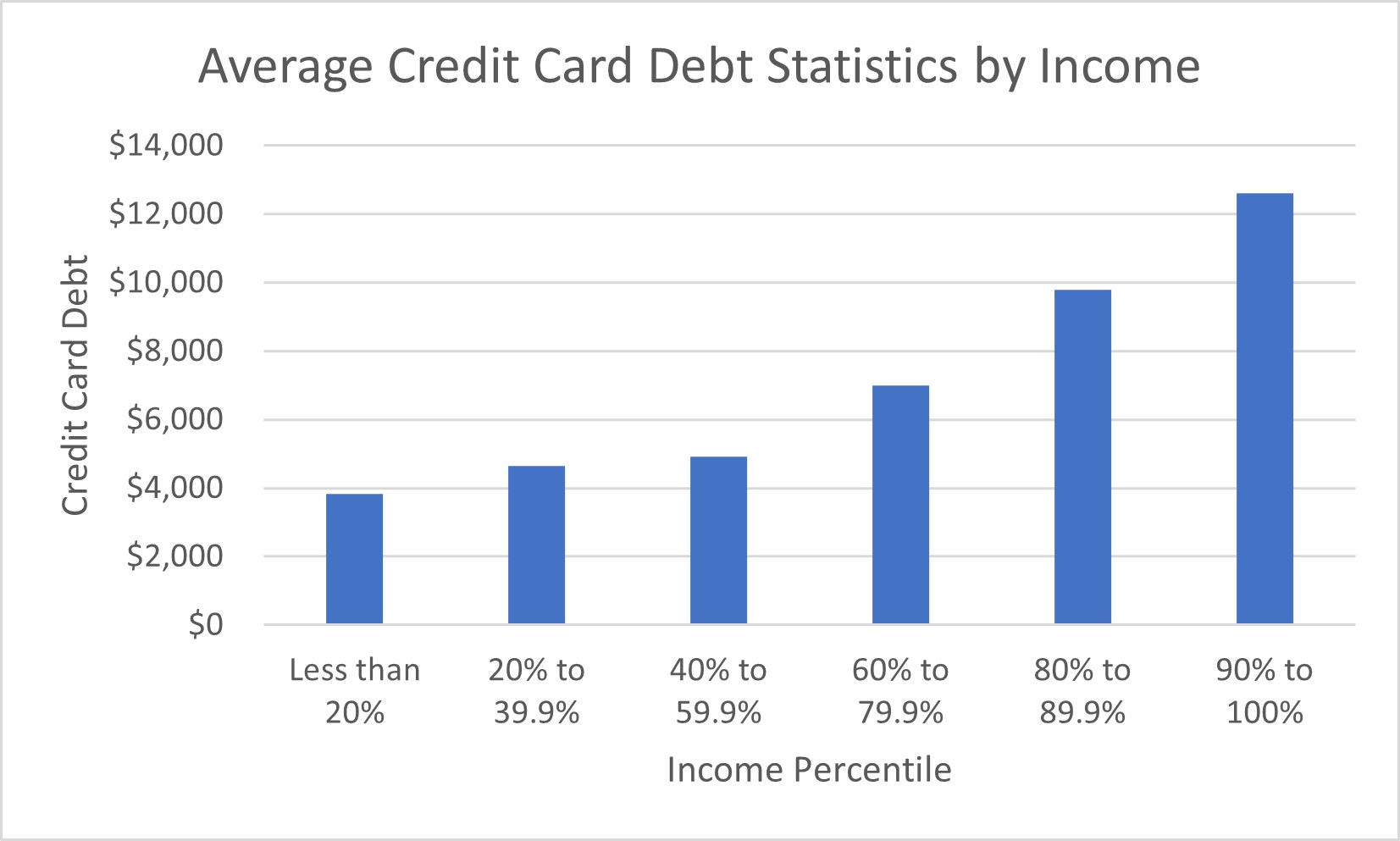

Those who make more money will likely have larger amounts of debt. That's what the data shows us in the following chart that shows the average debt amount of debt by income percentile.

Source: Lexington Law

It should be noted that while those who make more owe more, it may be easier for them to pay off their debt. High earners have usually have a lower debt-to-income ratio.

What are some reasons why people end up in credit card debt? Careless spending and shopping can contribute to large amounts of debt, which can make it difficult to pay off in time.

According to Lexington Law, the average American household had racked up $6,040 in debt, and the average credit card debt had increased by 9.4% since 2014. Read below to see the statistics.

Source: Lexington Law

Debt settlement occurs when borrowers are unable to make payments, and creditors accept a lower amount to avoid the risk of a borrower declaring bankruptcy. Consumers will need to make monthly payments to an escrow bank account until there is enough money for the debt settlement company to negotiate a deal with creditors. Consumers who go through and complete a debt settlement program reduce their debt by 45%.

More debt settlement statistics:

Source: NCES

While it may seem like it is impossible to escape your debt, you should know that it is possible to never have it, if you spend your money wisely. But once you do, it can be difficult to repay it. It can also affect your credit score if you are having trouble making payments on time, which can, later on, affect your chances of buying a home or making large purchases. If you cannot repay your debt, you may need to apply for a credit card settlement. It is crucial that you keep track of your expenses so that you are not struggling in the long run.

Things to know about your debt:

At the end of the day, it is about how you manage your money and how you choose to repay your loans and debt. We often spend more than we make and fail to understand the consequences until we are charged with a massive bill we cannot pay off all at once. Paying attention to your spending habit and making smart financial decisions is the best way to ensure that you will not incur large amounts of debt and can save up for important expenses and investments for the future.